London, November 10 2021

The International Gas Union (IGU), in partnership with the Oxford Institute for Energy Studies (OIES), today releases its inaugural Global Renewable and Low-Carbon Gas Survey Report. The world is about to choose the next step on the path which started in Paris and is about to leave Glasgow. Following COP26, it is apparent that ambitious global targets need to be matched with practicable action to ensure delivery. A major area of policy commitments & development has been focused on how to create viable global low-or-zero carbon hydrogen and renewable gas markets.

While natural gas, which currently provides around 25% of global primary energy supply, is the lowest carbon fossil fuel, there is growing recognition of the importance of low-carbon gases (biogas; biomethane, also known as renewable natural gas, and low-carbon hydrogen) as vital additional decarbonisation actors. The International Gas Union, working together with the Oxford Institute for Energy Studies and its partners from Imperial College London, University of Texas, Austin made the decision to create this global renewable gas database project to track development of low-carbon and renewable gas supply around the world.

“We made the choice to launch this report to demonstrate our support and appetite for the accelerated growth of the global renewable and low-carbon gas sector. However, there is limited transparency as regards volume and pricing when compared to other energy commodities. Developing effective growth strategies, requires an understanding of the baseline, and that is what we aim to establish with this series. It will track the industry’s progress, as it grows and develops over time” – Joe Kang, President IGU

For this first edition of the report, we used a combination of data collected in the survey and the project team’s own benchmarking work to assess the state of play in global renewable and low-carbon gases. The primary conclusions of the report are:

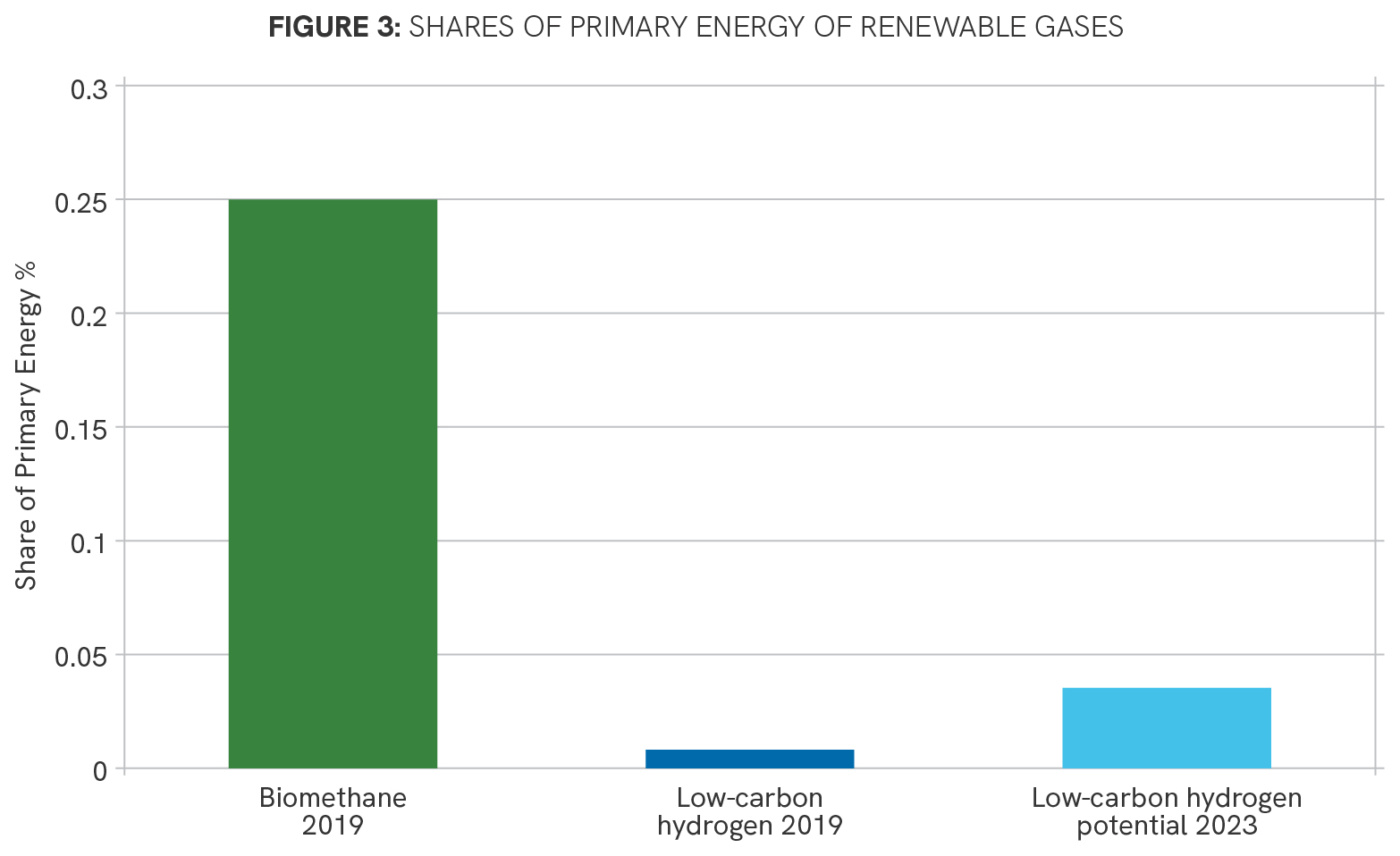

- Total global production of both biogas and biomethane is approx. 400 TWh, or approx. 1% of total global natural gas production. Over half of this production is concentrated in a few countries in Europe, with a further 25% in China.

- While sustainable biogas production potential could replace about 20% of the current global natural gas demand, according to the IEA, the current production pipeline is 20 times smaller.

- The production level for low-carbon hydrogen is also low at approx 0.5% of current hydrogen production, that is only approx 0.03% of global natural gas production. Despite significant focus on the role of hydrogen in the transition around the world, there has been only a very small increase in low-carbon hydrogen output in the last 5 years.

- A stronger policy focus on increasing production of low-carbon hydrogen is a vital driver for future growth in hydrogen project pipeline.

- Green hydrogen is significantly more expensive than any other form of renewable gas, but as the costs of both renewable electricity and electrolysers decrease over time, costs are expected to fall. In the meantime, blue hydrogen provides the most cost-effective and commercially ready source of this clean fuel.

- There is much stronger interest among policy makers and the broader commentariat in low-carbon hydrogen rather than biomethane. However, the the current levels of production (much more biogas) and the relative costs of biomethane and hydrogen suggest that it is important to raise biomethane up the near-term policy agenda.

- Given the scale of the decarbonisation challenge, and the need for as many workable solutions as possible to ease the pains of a global energy transition, all forms of renewable gas should be pursued as quickly as possible. This will require strong and clear policy support from governments globally, robust entrepreneurial initiative from the incumbent industry players and disruptors alike.

- Access to capital is of vital importance if these projects are to get to a viable global market. From non-commercial R&D seed funding all the way through to commercial debt finance and liquidity provision.

“The current level of planned and installed production capacity for renewable and low-carbon gases appears negligible compared to the stated plans, and that must be changed. This report is a call to action on all fronts – policy, industry, and the financial community. We all need to play our part if there really will be a practicable gaseous energy revolution.” — Joe Kang, President IGU

“The Oxford Institute for Energy Studies (OIES), together with its partners in this project from the Sustainable Gas Institute, Imperial College, London and the Bureau of Economic Geology, University of Texas, Austin, has been delighted to work with the International Gas Union on the production of this Global Renewable and Low-Carbon Gas survey report.

While we recognise that this first edition has only be based on limited data, it has already produced some valuable insights, and we expect this to grow further as the data coverage increases in future editions.” — Martin Lamber, OIES